This is one of several metrics that companies and investors use to make data-driven decisions about their business. As with other figures, it is important to consider contribution margins in relation to other metrics rather than in isolation. Alternatively, companies that rely on shipping and delivery companies that use driverless technology may be faced with an increase in transportation or shipping costs (variable costs). These costs may be higher because technology is often more expensive when it is new than it will be in the future, when it is easier and more cost effective to produce and also more accessible. A good example of the change in cost of a new technological innovation over time is the personal computer, which was very expensive when it was first developed but has decreased in cost significantly since that time. The same will likely happen over time with the cost of creating and using driverless transportation.

Contribution margin vs. gross margin

Now that you are familiar with the format of the CVP/Contribution Margin analysis, we’ll be using it to perform a number of what-if scenarios, but first, check your understanding of the contribution margin. The calculation of the contribution margin ratio is a three-step process. We explain its formula, differences with gross margin, calculator, along with example and analysis. You may also look at the following articles to enhance your financial skills. If the company realizes a level of activity of more than 3,000 units, a profit will result; if less, a loss will be incurred. Aside from the uses listed above, the contribution margin’s importance also lies in the fact that it is one of the building blocks of break-even analysis.

How confident are you in your long term financial plan?

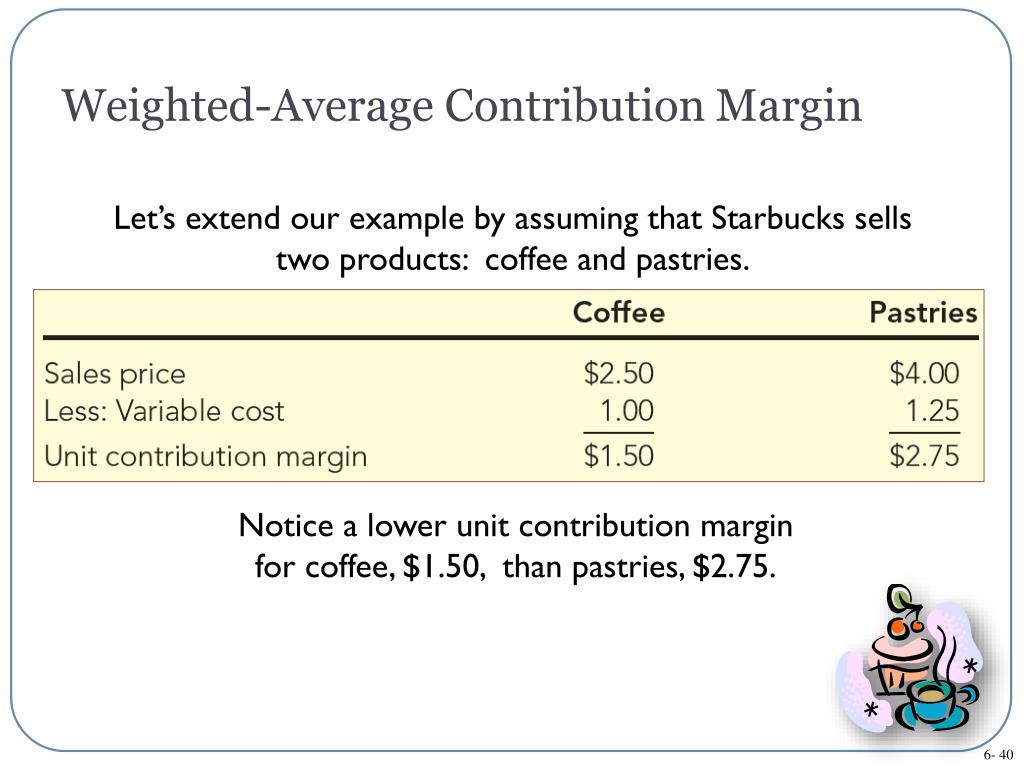

The contribution margin is the leftover revenue after variable costs have been covered and it is used to contribute to fixed costs. If the fixed costs have also been paid, the remaining revenue is profit. You can calculate the contribution margin by subtracting the direct variable costs from the sales revenue.

- A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

- Overall, per unit contribution margin provides valuable information when used with other parameters in making major business decisions.

- Fixed costs are costs that are incurred independent of how much is sold or produced.

- The higher the percentage, the more of each sales dollar is available to pay fixed costs.

- Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs.

Would you prefer to work with a financial professional remotely or in-person?

Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own.

How is contribution margin calculated?

Any remaining revenue left after covering fixed costs is the profit generated. However, the growing trend in many segments of the economy is to convert labor-intensive enterprises (primarily variable costs) to operations heavily dependent on equipment or technology (primarily fixed costs). For example, in retail, many functions that revenue recognition were previously performed by people are now performed by machines or software, such as the self-checkout counters in stores such as Walmart, Costco, and Lowe’s. Since machine and software costs are often depreciated or amortized, these costs tend to be the same or fixed, no matter the level of activity within a given relevant range.

What is the approximate value of your cash savings and other investments?

An increase like this will have rippling effects as production increases. Management must be careful and analyze why CM is low before making any decisions about closing an unprofitable department or discontinuing a product, as things could change in the near future. The contribution margin is calculated at both the unit level and the overall level. These examples demonstrate how this concept is applicable across a wide range of industries and can be an essential tool in pricing decisions, cost control, and profitability analysis. Understanding and applying this concept, helps enable businesses to make informed decisions that can enhance profitability and long-term success.

Suppose you’re tasked with calculating the contribution margin ratio of a company’s product. The formula to calculate the contribution margin ratio (or CM ratio) is as follows. In short, profit margin gives you a general idea of how well a business is doing, while contribution margin helps you pinpoint which products are the most profitable. Alternatively, the company can also try finding ways to improve revenues. However, this strategy could ultimately backfire, and hurt profits if customers are unwilling to pay the higher price.

Companies should supplement it with other financial and non-financial metrics to make comprehensive and well-informed decisions. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. 11 Financial is a registered investment adviser located in Lufkin, Texas.

Total contribution margin (TCM) is calculated by subtracting total variable costs from total sales. Overall, per unit contribution margin provides valuable information when used with other parameters in making major business decisions. Similarly, we can then calculate the variable cost per unit by dividing the total variable costs by the number of products sold. Only two more steps remain in our quick exercise, starting with the calculation of the contribution margin per unit – the difference between the selling price per unit and variable cost per unit – which equals $30.00.

However, the contribution margin facilitates product-level margin analysis on a per-unit basis, contrary to analyzing profitability on a consolidated basis in which all products are grouped together. Profits will equal the number of units sold in excess of 3,000 units multiplied by the unit contribution margin. The contribution margin ratio is calculated as (Revenue – Variable Costs) / Revenue. Very low or negative contribution margin values indicate economically nonviable products whose manufacturing and sales eat up a large portion of the revenues. Instead of doing contribution margin analyses on whole product lines, it is also helpful to find out just how much every unit sold is bringing into the business. Calculate the company’s contribution margin for the period and calculate its breakeven point in both units and dollars.